CamaPlan: Unique Highlights Overview

CamaPlan is a self-directed IRA administrator that empowers investors to diversify their retirement portfolios beyond traditional assets. Here are some unique highlights of CamaPlan:

Find the Best Gold IRA Company of Your State

Diverse Investment Options

CamaPlan allows investments in a wide array of asset classes, including:

- Real Estate: Direct ownership of residential or commercial properties.

- Precious Metals: Investments in gold, silver, and other approved metals.

- Private Placements: Opportunities in private companies and startups.

- Mortgage Notes: Investing in promissory notes secured by real estate.

- Tax Liens: Purchasing liens placed on properties due to unpaid taxes.

This flexibility enables investors to tailor their portfolios according to their expertise and interests.

Educational Resources

CamaPlan emphasizes investor education through:

- Cama Academy: Offers articles, videos, webinars, and seminars covering various investment topics.

- Self-Directed Investing Toolkit: Provides pro-tips and strategies to help investors achieve their financial goals.

These resources are designed to empower clients to make informed investment decisions.

Transparent Fee Structure

CamaPlan offers a clear and straightforward fee schedule:

- Account Setup Fee: A one-time fee of $50.50.

- Annual Maintenance Fees: Determined based on the type of account and assets held.

- Transaction Fees: Applied to specific actions, such as buying or selling assets within the IRA.

This transparency helps investors understand the costs associated with their accounts.

Personalized Client Services

As a regional firm, CamaPlan offers personalized services, including:

- Direct Access to Specialists: Clients can consult with knowledgeable professionals for guidance.

- Tailored Investment Strategies: Assistance in developing investment plans that align with individual goals.

This personalized approach ensures that clients receive support tailored to their unique needs.

Compliance and Custodial Oversight

CamaPlan ensures adherence to IRS regulations by:

- Custodial Oversight: Managing and administering self-directed IRA accounts in compliance with IRS rules.

- Guidance on Prohibited Transactions: Educating clients to avoid transactions that could jeopardize the tax-advantaged status of their accounts.

This focus on compliance helps safeguard clients’ retirement savings.

By offering diverse investment options, robust educational resources, transparent fees, personalized services, and strict compliance oversight, CamaPlan provides a comprehensive platform for investors seeking to take control of their retirement planning through self-directed IRAs.

Who are the People Behind CamaPlan?

CamaPlan, a self-directed IRA administrator, was founded by veteran investors Carl Fischer and Maggie Polisano. Their combined expertise has established CamaPlan as a reputable firm in the self-directed retirement account industry.

Carl Fischer

- Background: Carl Fischer is a third-generation real estate developer. He began his investment journey in the 1970s while working as a rocket scientist at the Kennedy Space Center. He holds a degree from Cornell University.

- Experience: With over 25 years in various investment sectors, Carl has overseen real estate transactions exceeding $20 million, including residential and commercial properties, mortgages, notes, and other obligations. His diverse background encompasses business, finance, technology, scheduling, and overall management.

- Certifications: Carl is a Certified IRA Services Professional (CISP) and a Certified Trust Specialist (CTS). He is also a certified real estate and continuing education instructor.

Maggie Polisano

- Background: Maggie Polisano is also a third-generation real estate developer and a graduate of Villanova University.

- Experience: Maggie has substantial experience in residential property development and investing, particularly in New Jersey, Pennsylvania, and Florida. She has a proven track record of executing profitable real estate transactions and provides clients with guidance on real estate planning, tax avoidance strategies, and general investing.

- Certifications: Maggie is a Certified IRA Services Professional (CISP) and a Certified Trust Specialist (CTS).

Under their leadership, CamaPlan has become synonymous with expertise, flexibility, responsiveness, and a diverse range of investment choices in self-directed retirement accounts. The firm’s commitment to investor education and personalized service reflects the founders’ dedication to empowering clients in their financial endeavors.

Does CamaPlan Offer Gold IRA Services?

Yes, CamaPlan offers Gold IRA services, enabling investors to include physical precious metals like gold within their self-directed Individual Retirement Accounts (IRAs). Here’s how their Gold IRA services work:

Account Setup

- Open a Self-Directed IRA: Begin by establishing a self-directed IRA with CamaPlan, which allows for a broader range of investment options, including precious metals.

Funding the Account

- Transfers and Rollovers: Fund your self-directed IRA through transfers or rollovers from existing retirement accounts, such as 401(k)s or traditional IRAs.

Selecting Precious Metals

- Approved Metals: CamaPlan permits investments in IRS-approved precious metals, including gold, silver, platinum, and palladium. These metals must meet specific fineness standards to qualify for inclusion in an IRA. citeturn0search6

Purchase Process

- Choose a Dealer: Select a reputable precious metals dealer to purchase the desired metals.

- Coordinate with CamaPlan: Complete the necessary forms, such as the Precious Metals Asset Purchase Form, and coordinate with CamaPlan to facilitate the purchase within your IRA. citeturn0search6

Storage

- IRS-Approved Depository: The IRS requires that physical metals in an IRA be stored in an approved depository. CamaPlan coordinates the storage of your metals in a secure facility, ensuring compliance with IRS regulations. citeturn0search6

Fees

- Transparent Fee Structure: CamaPlan offers a clear fee schedule, including account setup fees, annual maintenance fees, and transaction fees related to the purchase and storage of precious metals. Specific fees may vary based on the value of assets and the number of transactions.

Reporting and Compliance

- Account Statements: Receive regular statements detailing your holdings and account activity, ensuring transparency and compliance with IRS reporting requirements.

Liquidation

- Selling Metals: When you choose to liquidate your precious metals, CamaPlan facilitates the sale, ensuring that proceeds are correctly deposited back into your IRA or distributed as per your instructions.

By offering Gold IRA services, CamaPlan provides investors with the opportunity to diversify their retirement portfolios through the inclusion of physical precious metals, potentially enhancing portfolio stability and serving as a hedge against economic volatility.

What Products Can You Purchase at CamaPlan?

CamaPlan is a self-directed IRA administrator that offers investors the flexibility to diversify their retirement portfolios beyond traditional assets. Here’s an overview of the investment products you can purchase through a CamaPlan self-directed IRA:

Real Estate

- Types of Properties: Invest in single-family homes, multi-unit residences, apartment buildings, co-ops, condominiums, commercial properties, vacation homes, and unimproved land.

- Investment Strategies: Properties can be held for rental income, appreciation, or both. There’s no time limit on property holdings; they can be flipped for quick profits or maintained long-term.

Precious Metals

- Eligible Metals: Include IRS-approved metals such as gold, silver, platinum, and palladium in your IRA.

- Benefits: Precious metals can act as a hedge against inflation and economic volatility.

Mortgage Notes

- Lending Opportunities: Your IRA can function like a bank, lending money through secured or unsecured notes.

- Control: You determine the borrower, principal amount, interest rate, term length, and payment schedule.

Private Placements

- Investment Vehicles: Invest in private companies, startups, limited partnerships, and other private entities.

- Potential: These investments can offer high returns but come with increased risk and require thorough due diligence.

Tax Liens

- Acquisition: Purchase tax liens sold by counties, which are attached to real estate properties with unpaid taxes.

- Returns: Earn interest on the lien and potentially obtain the property title if the lien isn’t repaid.

Other Investments

- Commodities: Invest in physical goods like oil, gas, timber, and mineral rights.

- Foreign Currencies: Engage in forex trading within your IRA.

- Hedge Funds and Futures: Access more sophisticated investment strategies through hedge funds and futures contracts.

- Additional Options: Invest in account receivables, equipment leases, U.S. Treasury bills, trailers/trailer parks, and livestock.

Considerations

- Due Diligence: It’s crucial to thoroughly research and understand each investment type, as alternative assets can carry higher risks and may have less liquidity compared to traditional investments.

- IRS Regulations: Ensure all investments comply with IRS rules to maintain the tax-advantaged status of your IRA.

- Consult Professionals: Seek advice from financial advisors or tax professionals to align your investment choices with your retirement goals and risk tolerance.

By offering a broad spectrum of investment options, CamaPlan enables investors to tailor their retirement portfolios to their individual preferences and financial objectives.

CamaPlan Fees and Pricing:

CamaPlan offers a transparent and flexible fee structure for its self-directed IRA services, allowing clients to choose between different pricing options based on their investment preferences. Below is a detailed breakdown of the fees and pricing associated with CamaPlan accounts:

Account Setup Fee

- One-Time Fee: A $75 fee is charged upon the establishment of a new account.

Annual Maintenance Fees

Clients can select between two fee structures:

- Option A – Asset-Based Fee:

- Fee: $300 per asset held in the account, assessed annually.

- Applicability: Suitable for accounts with a limited number of assets.

- Example: An account holding two assets would incur an annual fee of $600.

- Option B – Value-Based Fee:

- Fee Calculation: Based on the highest account value during the annual term, with a minimum fee of $165 and a maximum of $2,020.

- Fee Schedule:

- $0 to $20,000: 0.94% of account value

- $20,001 to $80,000: 0.72%

- $80,001 to $180,000: 0.61%

- $180,001 to $300,000: 0.50%

- $300,001 to $500,000: 0.39%

- $500,001 and up: 0.33%

- Applicability: Ideal for accounts with higher values or multiple assets.

- Example: An account with a value of $60,000 would incur an annual fee of approximately $432 (0.72% of $60,000).

Transaction Fees

- Real Estate Transactions: $175 per transaction (purchases, sales, exchanges, transfer of asset).

- Other Transactions: $150 per transaction (purchases, sales, redemptions, exchanges, distributions, and transfer of assets).

- Wire Transfers:

- Domestic Incoming: $10

- Domestic Outgoing: $30

- International: $95

- ACH Transfer: $10 per transaction.

- Custodial Account Check: $10 per check issued.

- Cashier’s Check: $45 (includes overnight courier).

- Partial Transfer Out: $75 per transfer.

- Early Distribution: $150 per distribution.

Special Handling Fees

- Returned Bank Check: $50 per occurrence.

- Stop Payment: $50 per request.

- Declined/Refunded Credit Card: $50 per occurrence.

- Invalid Payment Method: $50 per occurrence.

- Late Charges on Past Due Invoices: $30 per late payment.

- Invalid Contact Information: $100 per occurrence.

- Expediting Documents/Transactions: $150 per request.

- Notary or Medallion Stamp: $10 per service.

- Overnight Courier: $35 per shipment (contingent on carrier pricing).

- 2-Day Courier: $25 per shipment (contingent on carrier pricing).

- Voided Check: $10 per check.

- Unidentified Incoming Funds: $25 per occurrence.

Processing Fees

- Obtain TIN/EIN for IRA/401K: $99 (processed by a third-party CPA).

- Direct Registration of Stocks (Per Stock): $50 per stock.

- Account Termination: $150 (includes transfer out).

- Incomplete Documents: $100 per hour (applies to investments, deposits, expenses, distributions, special services, research, copying).

Precious Metals Accounts

- Annual Maintenance Fee: Value-based, ranging from $160 to $280 annually.

- Storage and Insurance Fees: Calculated by multiplying the value of precious metals by 0.15%, paid annually in January.

Payment Methods

- Accepted Forms: Fees can be paid via credit card, debit card, or bank account.

- Credit Card Transactions: Subject to a 3.5% convenience fee.

Minimum Cash Balance Requirement

- Requirement: Accounts must maintain a minimum cash balance equivalent to two years of annual fees.

- Example: For an asset-based annual fee of $300 per asset, an account with one asset must maintain a minimum balance of $600.

Additional Considerations

- Fee Selection: Clients must select either the asset-based or value-based fee option upon account setup.

- Fee Changes: CamaPlan reserves the right to modify fees with 30 days’ advance notice.

- Non-Payment Consequences: Failure to pay fees may result in asset liquidation to cover

What Do CamaPlan Reviews Say?

CamaPlan, a self-directed IRA administrator, has received various ratings and reviews across multiple platforms. Here’s an overview of their evaluations:

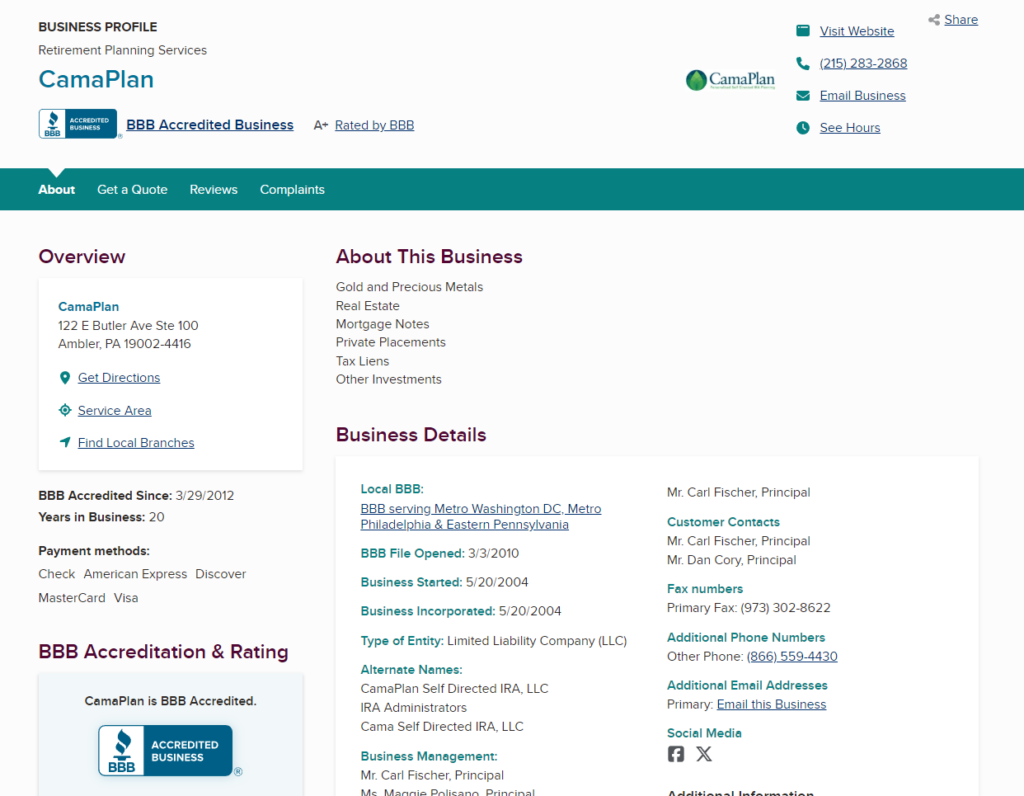

Better Business Bureau (BBB)

- Accreditation: CamaPlan has been accredited by the BBB since March 30, 2012.

- Rating: The company holds an A+ rating, indicating a strong commitment to resolving customer complaints and maintaining transparent business practices. citeturn0search6

Google Reviews

- Average Rating: CamaPlan has a 3.5 out of 5-star rating on Google, based on 10 customer reviews.

- Customer Feedback: Many reviews highlight positive experiences, particularly praising the knowledgeable team and good customer service.

Birdeye

- Average Rating: CamaPlan holds a 3.6 out of 5-star rating on Birdeye, based on 14 reviews.

- Customer Experiences: Reviews are mixed, with some clients appreciating the personalized service, while others express concerns about fees and account management.

Chamber of Commerce

- Average Rating: CamaPlan has a 3.4 out of 5-star rating, based on 12 reviews.

- Client Testimonials: Feedback varies, with some clients commending the company’s assistance in real estate investments, while others mention issues related to fees and customer service interactions.

Glassdoor

- Employee Insights: CamaPlan has a 3.9 out of 5-star rating on Glassdoor, based on 5 employee reviews.

- Work Environment: Employees provide mixed feedback, reflecting diverse experiences within the company.

CamaPlan maintains a strong A+ rating with the BBB, reflecting effective handling of customer concerns. Customer reviews on platforms like Google, Birdeye, and the Chamber of Commerce present a range of experiences, with average ratings between 3.4 and 3.6 out of 5 stars. Common praises include knowledgeable staff and personalized service, while some concerns are raised regarding fees and account management.

Why aren’t There Many CamaPlan Complaints?

There are several reasons why CamaPlan has relatively few complaints compared to other self-directed IRA custodians. Here’s an in-depth look at why CamaPlan maintains a lower complaint volume:

Niche Market with a Specialized Clientele

- CamaPlan specializes in self-directed IRAs (SDIRAs), which cater to a specific type of investor—those looking to diversify into real estate, private placements, precious metals, and other alternative investments.

- Since their clients are usually experienced investors who understand self-directed IRAs, they are less likely to file complaints over standard industry issues.

Personalized Customer Service

- Unlike larger firms that use call centers and automated systems, CamaPlan provides personalized account management.

- Clients often work directly with knowledgeable professionals rather than going through multiple customer service layers.

- Direct communication helps resolve issues quickly, preventing complaints from escalating into public grievances.

Transparent Fee Structure

- Flat Annual Fees: Unlike other IRA custodians who charge fees based on account value, CamaPlan offers a flat-rate fee structure, preventing confusion or unexpected charges.

- Published Fee Schedule: Their fees are listed openly on their website, reducing surprises that often lead to customer dissatisfaction.

- Clients Are Informed Upfront: Many complaints in the financial industry stem from hidden fees, but CamaPlan’s clear structure minimizes this issue.

Strong Focus on Investor Education

- Cama Academy: Provides educational resources, webinars, and workshops to help clients fully understand self-directed investing.

- Investor Toolkit: Offers step-by-step guidance on using SDIRAs effectively.

- Since informed clients are less likely to experience confusion or frustration, there are fewer complaints.

Compliance with IRS Regulations

- Strict Adherence to IRS Guidelines: CamaPlan ensures that all self-directed IRA transactions comply with IRS rules and prohibited transaction laws.

- Expert Assistance on Tax Implications: Clients receive guidance to avoid mistakes that could lead to IRS penalties, reducing disputes related to tax issues.

Quick Issue Resolution

- Efficient Handling of Concerns: CamaPlan’s smaller, boutique structure allows them to handle issues quickly before they turn into complaints.

- Proactive Customer Service: The company likely resolves potential disputes internally rather than letting them escalate into formal complaints or negative reviews.

No Major Lawsuits or Scandals

- Some competitors in the self-directed IRA industry have been involved in lawsuits related to fraudulent investments, Ponzi schemes, or lack of due diligence—but CamaPlan does not have any major legal disputes.

- This clean record reinforces their reputation and reduces formal complaints.

Reputation Management & Word-of-Mouth Growth

- CamaPlan relies heavily on referrals from existing clients, rather than aggressive advertising.

- Their targeted client base means fewer public complaints, as most investors seek them out intentionally rather than signing up through high-pressure sales tactics.

Are There Any CamaPlan Lawsuits?

No.

We didn’t find any lawsuits involving this company.

Can You Trust Camaplan? Is Camaplan Legit?

Yes.

CamaPlan is a prominent and reliable name in the industry.

Whenever you’re curious about a company, just keep these points in mind:

Tip #1: Check Their Regulatory Compliance and Accreditation

Check for proper licensing and registration with relevant financial regulatory bodies such as the Securities and Exchange Commission (SEC) or Financial Industry Regulatory Authority (FINRA).

Verify the company’s accreditation with industry organizations like the Professional Coin Grading Service (PCGS) or the Numismatic Guaranty Corporation (NGC).

It will help you check how credible they are.

Tip #2: Look into The Company’s Background

- Research the company’s history, including years in business and any name changes.

- Examine the Better Business Bureau (BBB) rating and accreditation status.

- Review customer feedback on reputable third-party review sites like Trustpilot or Consumer Affairs.

Tip #3: Does the Company Offer Good Resources?

- Assess the clarity of information provided about fees, storage options, and buyback policies.

- Evaluate the quality and depth of educational resources offered to investors.

- Verify that the company provides clear information about IRS regulations regarding precious metals IRAs.

Tip #4: What are Their Product Offerings and Pricing?

- Ensure the company offers IRS-approved precious metals for IRA investments.

- Compare pricing with other reputable dealers to ensure competitiveness.

- Be wary of companies pushing numismatic or collectible coins over bullion for IRA investments.

Tip #5: Confirm the Storage and Custodian Partnerships

Verify that the company works with IRS-approved custodians and secure storage facilities. According to IRS’ regulations, you cannot store your gold IRA’s precious metals at your home.

You’ll need a certified third-party storage provider.

Check the company’s storage and custodian partner to ensure you’re working with a reliable firm. Moreover, ensure they offer segregated storage options for your precious metals.

Segregated storage means your owned precious metals products will be stored separately from other investors’ possessions. Similarly, non-segregated storage means your products will be stored along with others.

Keep in mind that storage providers charge extra for segregated storage.

Some popular custodians include Equity Trust and Goldstar Trust.

Red Flags to Watch For in Gold IRA Companies

- Promises of guaranteed returns or claims of “secret” investment strategies.

- Pressure to act immediately or make large investments without proper consideration.

- Lack of physical address or unclear company ownership structure.

- Unwillingness to provide detailed information about fees or policies in writing.

By thoroughly evaluating these aspects, investors can make an informed decision about the legitimacy and reliability of a gold IRA company. It’s crucial to conduct due diligence and, if necessary, consult with a financial advisor before making any investment decisions.

CamaPlan Review Summary:

Overall, CamaPlan seems like a decent choice for anyone interested in IRAs.

However, it’s always best to browse the market and see what others have to offer.

What are your thoughts on this company?

Let us know in the comments.